Investing for Beginners: Build Wealth Early

Index funds, Roth IRAs, compound interest — the strategies that actually work if you start in your 20s or 30s.

- The power of compound interest with real numbers

- Index funds vs. stock picking — what the data says

- Tax-advantaged accounts: Roth IRA, 401k, HSA

- The three mistakes that cost young investors the most

1. Compound interest: time is the real asset

Investing for Beginners: Build Wealth Early

Index funds, Roth IRAs, compound interest — the strategies that actually work if you start in your 20s or 30s.

Compound interest

Compound interest means your money earns returns, and then those returns earn returns too.

If you invest early, time does more of the work. That is why a 10-year delay can cost more than many people expect.

Real example

- 200 dollars per month

- 7 percent average annual return

- 30 years

- Future value: about 236,000 dollars

Wait 10 years to start, and the same plan is only about 113,000 dollars.

The gap comes from lost compounding years, not just lost contributions.

Why early dollars matter most

The first dollars you invest are like seeds. They have the longest runway to grow.

A late start can still work. But you need to save much more each month to catch up, because compounding has less time to act.

2. Index funds beat most stock pickers

Index funds vs. stock picking

An index fund owns many stocks at once. A stock picker owns a few and tries to choose winners.

For beginners, index funds usually win on three fronts:

- diversification

- low cost

- simplicity

What the data says

SPIVA reports have shown that most active U.S. equity funds underperform their benchmarks over long periods, especially after fees.

Why fees matter

A fund charging 0.03 percent per year leaves almost all of your money working. A fund charging 1 percent takes a much bigger slice over time.

That difference compounds too. Over 30 years, cost can matter almost as much as performance.

3. The tax shelters that accelerate growth

Tax-advantaged accounts

These accounts help you keep more of your returns.

Roth IRA

- Contributions are made with after-tax money

- Qualified withdrawals are tax-free

- 2024 limit: 7,000 dollars, or 8,000 dollars if age 50 or older

401k

- Contributions are usually pre-tax

- Growth is tax-deferred

- 2024 employee limit: 23,000 dollars, plus 7,500 dollars catch-up if age 50 or older

HSA

- Tax-deductible or pre-tax contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses

- Best used only if you have an HSA-eligible health plan

A simple priority order

- Get the full employer match in the 401k.

- Fund a Roth IRA if you qualify.

- Add more to the 401k or HSA.

The employer match is free money. Skipping it is like refusing part of your salary.

4. The three mistakes that hurt young investors most

The three costly mistakes

1. Waiting to start

Delaying investing reduces the number of compounding years.

2. Chasing hot stocks or trends

Past winners are not guaranteed future winners.

3. Ignoring fees and taxes

A small percentage can become a large dollar amount over decades.

A better system

Use automatic investing.

Set a monthly transfer. Buy broad index funds. Rebalance once or twice a year. That removes emotion from the process and makes good behavior easier to repeat.

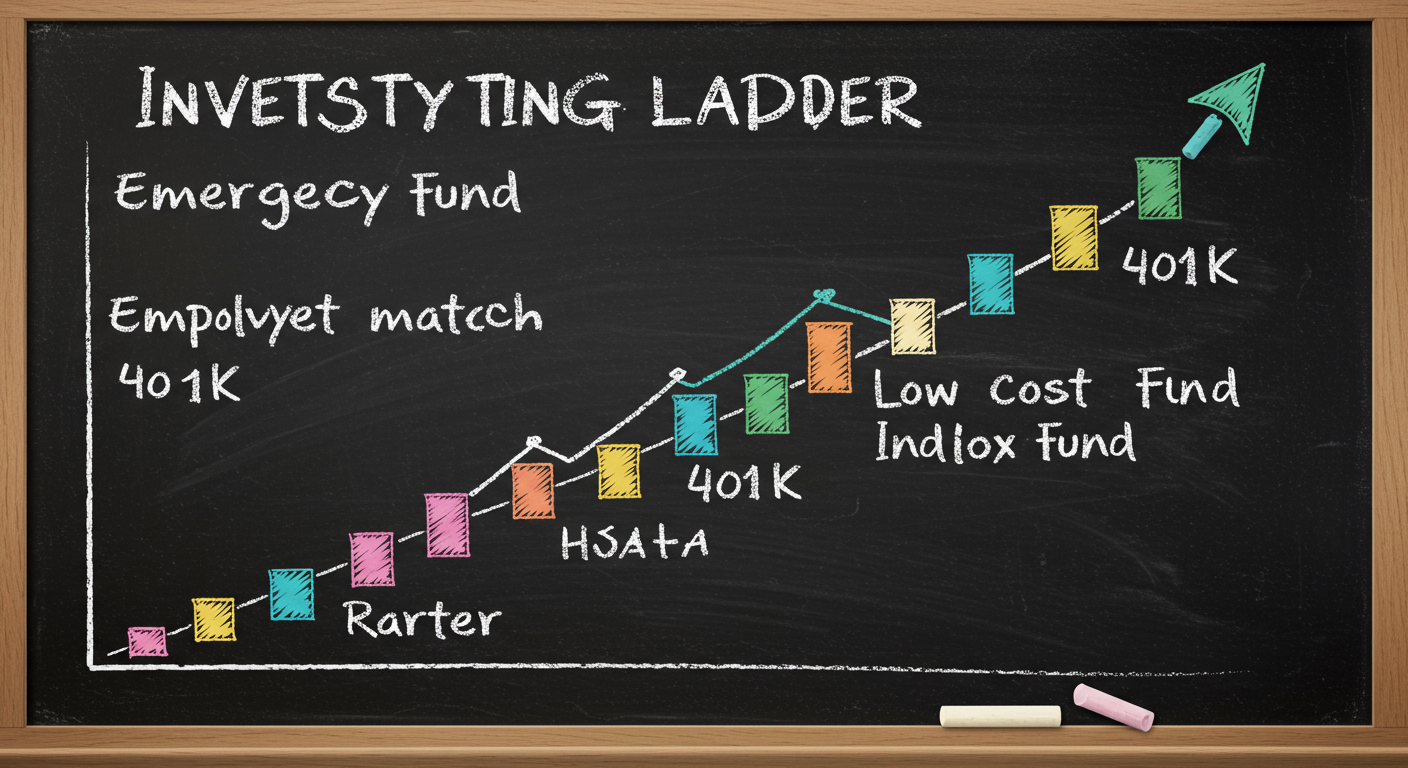

5. A practical starter plan for your 20s and 30s

A beginner investing plan

- Build a small emergency fund.

- Get the full 401k employer match.

- Invest in a low-cost index fund.

- Use a Roth IRA if you qualify.

- Use an HSA if you have an eligible health plan.

- Rebalance once a year.

Asset allocation

A mix like 80 percent stocks and 20 percent bonds can reduce panic selling for some beginners, but the right mix depends on your goals and risk tolerance.

The main takeaway

Start early. Keep costs low. Use tax-advantaged accounts. Own the market instead of trying to beat it.

That combination is plain, not flashy. It works because it gives time, discipline, and math room to do their job.

Keep going with Slate

Pick up where this left off in your own voice session.